Friday, November 21, 2014

Thursday, November 6, 2014

What Does Progressive Versus Conservative Matter? How About Survival Of The Species?

We're not the fastest. Nor the strongest. Nor the toughest. We lack sharp, pointy teeth and claws. But we learn. We figure out and understand. We develop new and better means to deal with our world and ourselves for our mutual benefit. We progress. It's our shtick.

It's what we do to survive ... or fail to do and decay.

Every time we fail to challenge science denialism, our species slips closer to oblivion. ...whether at our own hands or by failing to foresee and adapt to nature.

Every time racism or sexism goes un-chastised and is allowed to fester, our collective chances of making it through the next billion years drop a little bit.

Every time destructive notions that hurt our prosperity -- like Trickle Down -- get brought up without being smacked right back down, we slide a bit closer to the dustbin of species by squandering our potential.

Cuts to education funding don't just make it harder for our businesses to find a pool of qualified labor at reasonable cost. Cuts to education funding reduce our chances of survival versus what they could be.

Cuts to research funding don't just make it harder for our researchers to move their fields forward; they make it that much more likely that we'll lack sufficient findings to adapt to each new event.

Cuts to infrastructure funding don't just make the roads harder on our cars; they decrease the efficiency of our species ... an efficiency that will at times be sorely needed.

Our art, our culture, our science, our philosophy, our history, our understanding ... these aren't just niceties to enjoy as surplus, as if they were mere fringe benefits. These are necessities. Our survival builds from enlightenment. From progress. It lives on progressiveness.

Conservatives would tear down all that progressives have built and stand in the way of further progress. Robbing us of our species' strong suits. Leaving us more vulnerable to cataclysm.

So go ahead and stand up to that conservative loudmouth. It matters.

Wednesday, July 9, 2014

Inflation, Deflation, and Redistribution

As Paul Krugman points out in a couple of recent articles, it's worth considering whose interests are served by high interest rates and low inflation, or as Krugman calls it, hard-money ideology.

"Basically, inflation redistributes wealth down the scale of both wealth and age, while deflation does the reverse."See:

Tuesday, July 1, 2014

Friday, June 20, 2014

Tim Stuhldreher: Every year, we waste Spain

Tim Stuhldreher: Every year, we waste Spain: ... on the monumental accomplishment of American heatlhcare spending.

Thursday, April 3, 2014

Friday, March 28, 2014

The Retail Sales Gap Is The Housing Gap

Atif Mian and Amir Sufi pondered why spending hasn't caught up to trend.

How would spending catch up to trend when employment hasn't caught up to trend?

And why would we expect employment to catch up when home construction lurks below the 1982 recession levels let alone below trend?

And even if employment were caught up, we're not going to have as much retail sales of home furnishings and such household goods until we have as many new homes to furnish.

Notice how in the early 1980s, home construction started up before employment. Just like how in 2006 home construction started slowing before employment ... and then started plummeting before employment.

Retail sales include paint, furnishings, and lots of other household goods. So really, is it any surprise that retail sales haven't recovered to trend but rather have only stopped dropping?

By and large, the home is where the retail sales live.

And why would a home builder ramp up construction when employment is low? Why is it again that we haven't restored the CCC and WPA this time around to get people working?

How would spending catch up to trend when employment hasn't caught up to trend?

And why would we expect employment to catch up when home construction lurks below the 1982 recession levels let alone below trend?

And even if employment were caught up, we're not going to have as much retail sales of home furnishings and such household goods until we have as many new homes to furnish.

Notice how in the early 1980s, home construction started up before employment. Just like how in 2006 home construction started slowing before employment ... and then started plummeting before employment.

Retail sales include paint, furnishings, and lots of other household goods. So really, is it any surprise that retail sales haven't recovered to trend but rather have only stopped dropping?

By and large, the home is where the retail sales live.

And why would a home builder ramp up construction when employment is low? Why is it again that we haven't restored the CCC and WPA this time around to get people working?

Thursday, March 27, 2014

What Came First: The Decline In Housing Or The Mortgage Crisis?

We're awash in a great sea of complicated answers to the question of what caused the Lesser Depression. Why? The story's rather simple.

For those who would say it all comes down to deregulation, the repeal of Glass-Steagall, and sub-prime loans, please answer this: How could a collapse in loans that comes well after the sharp drop in housing starts supposedly reach back in time and cause that preceding sharp drop in housing starts? Or how could failures of financial institutions travel time to kick off the decline in housing starts before they started failing?

The delinquency rate on single family residential mortgages averaged 2.2% between 1991 and 2007. Let's presume that wasn't a time of extraordinary caution and thus that 2.2% represents a reasonably ordinary rate of delinquencies. That rate dipped below 2 in 2003 and didn't get back up to 2 until the fourth quarter of 2006. Delinquencies didn't climb past 2.2% until the 2nd quarter of 2007, over a year after housing starts began plummeting. It seems quite clear that since there was no rash of delinquencies until well after housing starts crashed, we can't reasonably blame the decline in starts on the delinquencies. In other words, failing sub-prime loans simply don't work as an explanation without time travel.

Bank failures run a similar course. None in 2006 while housing starts drop sharply. Three in 2007. But 25 in 2008. Housing starts fell off the cliff long before banks started failing.

But then, what did go along with the housing starts decline? Why did they stop starting so many? Could it be that folks stopped being willing to pay ever higher prices?

Yep. In early 2006, housing prices tapered, peaked, and then started dropping a bit. And then they went flat for a while. Sellers resisted selling for less than they'd hoped a few months earlier. It's easy to understand reluctance to drop prices when it had so recently been a sellers market. But before long, prices joined in at the same angle of descent they'd set up in housing starts. Of course those two declines would feed into each other. With prices no longer rising and worse declining, it just doesn't make sense to build as much.

And what happens when we don't build as many houses? There's a bit of lag in effect. After all, once a start happens there's usually a few months of building. But as some months go by with a continuing sharp drop in house component orders and furniture sales, we get a decline in employment.

And once we have a decline in employment, fewer people can afford houses and fewer people can hold off on selling houses ... at any price.

In short order, not long after employment started down from the October 2006 peak, the bottom fell out from under house prices after March 2007.

Which brings us to the 2nd quarter of 2007. Remember that? That was when delinquencies started up past the norm for the preceding decades. So here's the question: did all this happen because collapsing sub-prime loans hopped a ride on Dr. Emmett Brown's DeLorean back to before the home prices, housing starts, and unemployment all started down? Or should we perhaps consider that maybe reality actually went in chronological order?

What came first? Home prices stopped rising and housing starts fell. Then unemployment. And we don't get into issues with mortgage-backed securities and complex derivatives until after those three got together. Can someone show us a working time machine or reference to all of this in Nostradamus? If not, no matter how much sub-prime loans and Glass-Steagall's repeal might have made the aftermath worse, it might make sense to presume they didn't have a thing to do with causing the whole mess.

Tuesday, March 25, 2014

When Higher Labor Costs Increase Sales Volume

There's this notion, "Lower labor costs are good for the rich." So some say.

Partly. In micro, yes. In macro, no. Directly and individually, yes. Indirectly and in aggregate, no.

Imagine if my company A sells widgets and competing company B sells widgets and companies C-Z sell other things but not widgets and the employees of companies C-Z buy widgets from A and B. If I unilaterally raise the wages 10% within company A but B doesn't follow suit, that's bad for my relative profit margin. (And it raises the question of whether B's larger profit margin is of more advantage then my potential increased worker loyalty and morale ... which could go either way.) But if all companies A-Z raise the wages, then A and B can both sell more widgets because the employees of companies C-Z have more money to spend.

When one company increases wages alone, it's playing a somewhat risky game. If workers feel more loyal and dedicated on account of the increase, that could boost production, reduce inventory shrinkage, and diminish costs from absenteeism and turnover. As a microcosm of the business world, the increasing company has to place a bet as to whether those advantages will make up for increased wage costs to keep profit margins as good as or better than those at competitors.

It's a different story when all companies engage in the same increase. The in-market competitive risk (seen in a unilateral increase) doesn't apply. Instead, since most products will have a lower mark-up to make up for wages than the amount of the wage increase, it's only a question of whether the increased wages of each company's customers boost sales volume and how much that boosts profits.

Partly. In micro, yes. In macro, no. Directly and individually, yes. Indirectly and in aggregate, no.

Imagine if my company A sells widgets and competing company B sells widgets and companies C-Z sell other things but not widgets and the employees of companies C-Z buy widgets from A and B. If I unilaterally raise the wages 10% within company A but B doesn't follow suit, that's bad for my relative profit margin. (And it raises the question of whether B's larger profit margin is of more advantage then my potential increased worker loyalty and morale ... which could go either way.) But if all companies A-Z raise the wages, then A and B can both sell more widgets because the employees of companies C-Z have more money to spend.

When one company increases wages alone, it's playing a somewhat risky game. If workers feel more loyal and dedicated on account of the increase, that could boost production, reduce inventory shrinkage, and diminish costs from absenteeism and turnover. As a microcosm of the business world, the increasing company has to place a bet as to whether those advantages will make up for increased wage costs to keep profit margins as good as or better than those at competitors.

It's a different story when all companies engage in the same increase. The in-market competitive risk (seen in a unilateral increase) doesn't apply. Instead, since most products will have a lower mark-up to make up for wages than the amount of the wage increase, it's only a question of whether the increased wages of each company's customers boost sales volume and how much that boosts profits.

Thursday, March 13, 2014

Not So Much With The Spending

Real government consumption expenditures and gross investment as a share of real GDP since 1950.

What We Should Have Done With The Banks (Hint: It Isn't Letting Them Collapse)

There are still people suggesting we should have let more banks collapse, apparently rekindled by discussions of Wall Street bonuses totaling more than the annual pay of all minimum wage workers.

Per Hyman Minsky in "Stabilizing an Unstable Economy",

We arguably should have required that in each bank to be bailed out all the major executives must be fired and thoroughly investigated ... as a condition of the bailout. That was the job that should have been done but wasn't.

Per Hyman Minsky in "Stabilizing an Unstable Economy",

"There is no possibility that we can ever set things right once and for all; instability, put to rest by one set of reforms will, after time, emerge in a new guise."And that applies to letting the free market wipe out banks rather than bailing them out as well. The utility of allowing such a collapse is minimal. After time, a way will be found to once again believe in risky investments and instability will reform, no matter how many banks were allowed to fail. Meanwhile, the harm of such a collapse is significant, as a bank's customers (including businesses with otherwise profitable models) experience financing shortfalls through no fault of their own when that bank goes belly up. And those innocent customers are often themselves wrongfully driven into failure by the failure of the bank. And that means lots of layoffs of otherwise productive workers, massive suffering on account of letting banks collapse.

We arguably should have required that in each bank to be bailed out all the major executives must be fired and thoroughly investigated ... as a condition of the bailout. That was the job that should have been done but wasn't.

Wednesday, March 12, 2014

The Output Gap Continues; The Impact Of Deficit-Hawks

The difference between "no longer getting worse" and "actually returning to normal":

We stopped getting worse. We still need a serious boost -- like from reversing the austerity of recent budget years -- to get back to good. Alternatively, a large enough boost to EITC could be another way of doing that while at the same time helping mitigate our ever-rising inequality.

Speaking of the recent austerity, here's that in a picture:

Had we not implemented such budget-cutting, deficit-hawk, austerity from 2010 (by not increasing spending commensurate with population growth) and even worse after (by actually reducing government consumption expenditures and gross investment), that alone would have at least had us significantly closer to potential by now. In other words, we'd have had more of a recovery.

We stopped getting worse. We still need a serious boost -- like from reversing the austerity of recent budget years -- to get back to good. Alternatively, a large enough boost to EITC could be another way of doing that while at the same time helping mitigate our ever-rising inequality.

Speaking of the recent austerity, here's that in a picture:

Had we not implemented such budget-cutting, deficit-hawk, austerity from 2010 (by not increasing spending commensurate with population growth) and even worse after (by actually reducing government consumption expenditures and gross investment), that alone would have at least had us significantly closer to potential by now. In other words, we'd have had more of a recovery.

If The Policies Were Worse, Explain Why The Outcome Is Better (And Vice Versa)

Timothy Taylor presents a challenge to "critics of the U.S. fiscal and monetary policies in the aftermath of the Great Recession". That challenge: "explain why, if the policies were so bad, the outcome has been comparatively so good."

Tuesday, March 11, 2014

Thoma on Capitalism, Inequality, Social Insurance, and Growth

From Mark Thoma writing in the Fiscal Times,

"Why is rising inequality a matter that our social insurance system should address? The idea behind insurance is to spread the costs of harmful events we cannot control across a large number of people. With fire insurance, for example, participants pool their money into a large sum, and the unlucky few that experience fires draw from the pool of money to cover their losses. In the end there is a redistribution of income from the winners who escape a fire to the unfortunate who don’t, but it would be wrong to view this as a net cost to the winners. The insurance premiums buy protection from fire – a benefit – and presumably the benefit exceeds the cost of the insurance.

...

At some point, one I believe we’ve passed already, the benefits of inequality in terms of incentives are surpassed by the costs. As Joseph Stiglitz argues, “Inequality leads to lower growth and less efficiency. Lack of opportunity means that its most valuable asset – its people – is not being fully used. Many at the bottom, or even in the middle, are not living up to their potential, because the rich, needing few public services and worried that a strong government might redistribute income, use their political influence to cut taxes and curtail government spending. This leads to underinvestment in infrastructure, education, and technology, impeding the engines of growth.”"

Tuesday, February 25, 2014

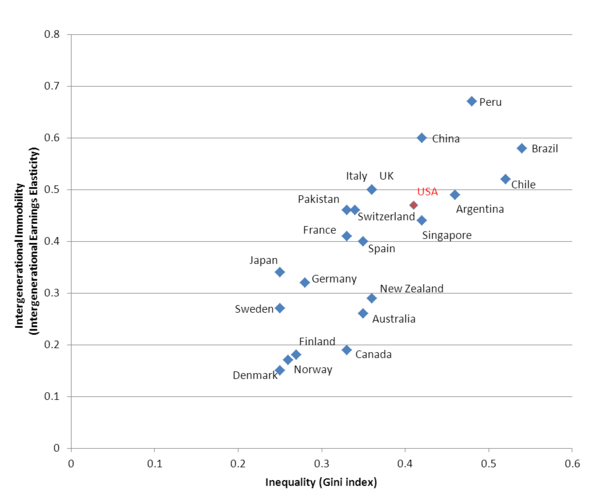

Mobility or Higher Standards?

"More important, in any capitalist society most people are bound to be part of the middle and working classes; public policy should focus on raising their standard of living, instead of raising their chances of getting rich. What made the U.S. economy so remarkable for most of the twentieth century was the fact that, even if working people never moved into a different class, over time they saw their standard of living rise sharply. ... Raising living standards for ordinary workers is hard: you need to either get wages growing or talk about things that scare politicians, like “redistribution” and “taxes.” But making it easier for some Americans to move up the economic ladder is no great triumph if most can barely hold on."

It's a strong point, one which Paul Krugman then takes up and restates more snappily with,

"if you want a society in which everyone has a decent life, you need to construct a society in which everyone has a decent life — not a society in which everyone has a small but equal chance of living the lifestyle of the rich and famous. ... Since anyone could find himself or herself downwardly mobile, social mobility arguably actually strengthens the case for a strong safety net."Mobility isn't all it's cracked up to be. It has downs with it's ups. Unlike an overall higher standard of living.

The American way is a melting pot or at least a mixing bowl, not a sieve.

The American way is a melting pot or at least a mixing bowl, not a sieve.

We may preserve elements rather than fusing into a homogeneous mass, but we mix. It's how we come up with our best, by exchanging ideas and forging something new.

This isn't the first time folks have fought against the melting pot. But those who fight it are just as wrong now as they were before. We gain much from being a harmonious mixture of different ingredients that stand together. Baking soda is great in a cookie; not so good on its own.

--

See also Paul Brandeis Raushenbush's "'Sincerely Held Religious Beliefs' and the Fraying of America" regarding "discriminatory and deeply un-American" legislation in Arizona.

We may preserve elements rather than fusing into a homogeneous mass, but we mix. It's how we come up with our best, by exchanging ideas and forging something new.

This isn't the first time folks have fought against the melting pot. But those who fight it are just as wrong now as they were before. We gain much from being a harmonious mixture of different ingredients that stand together. Baking soda is great in a cookie; not so good on its own.

--

See also Paul Brandeis Raushenbush's "'Sincerely Held Religious Beliefs' and the Fraying of America" regarding "discriminatory and deeply un-American" legislation in Arizona.

Thursday, February 13, 2014

College Versus Trade School: At What Cost These Technical Skills Come?

They're missing something, those like Robert Reich who would argue that we should worry less about four-year college and rally behind trade and technical schools as a low-cost alternative. Many of us who've been in the position of interviewer or boss are looking for someone with the critical thinking, creativity, and understanding fostered by general education in the humanities and basic sciences. It may be possible for a great candidate from a tech school to have that critical thinking on their own without that general education, but it's less likely.

Further, there's value beyond the directly vocational in the general education that comes with a bachelor's degree. More knowledge in the humanities and basic science makes for better citizens, a more informed electorate, and an all around improved society. While some very few attain such knowledge through self-study, on the whole we're more likely to get that from widespread college education. It truly is a public good and good for the general public.

Full college may not be for everyone. Trade and technical schools serve well to train workers who are not prepared for college. But if we confuse their playing a useful part with somehow replacing the benefits of expanded college graduation, we risk the reduction of potential for whole generations.

Further, there's value beyond the directly vocational in the general education that comes with a bachelor's degree. More knowledge in the humanities and basic science makes for better citizens, a more informed electorate, and an all around improved society. While some very few attain such knowledge through self-study, on the whole we're more likely to get that from widespread college education. It truly is a public good and good for the general public.

Full college may not be for everyone. Trade and technical schools serve well to train workers who are not prepared for college. But if we confuse their playing a useful part with somehow replacing the benefits of expanded college graduation, we risk the reduction of potential for whole generations.

Subscribe to:

Posts (Atom)